Recognizing the suitable shares is a ability that each investor must study, and the sheer quantity of market information, on the principle indexes, on particular person shares, on and from inventory analysts, can current an intimidating barrier. Thankfully, there are instruments to assist. The Smart Score is a knowledge assortment and collation device from TipRanks, utilizing an AI-powered algorithm to type the info on each inventory in keeping with a collection of things, 8 in all, which can be identified for his or her robust correlation with future share outperformance.

That each one feels like a mouthful, however it boils all the way down to this: a complicated information device that provides you a easy rating, on a 1 to 10 scale, to evaluate the prospects of any given inventory. It places the advanced world of inventory market information at your fingertips.

The Good 10, in fact, must be an excellent neon signal put up guiding buyers in for a better look – and typically, it guides buyers towards shares which have by no means lacked for headline or discover. These are a number of the market’s giants, shares which can be family names, characteristic trillion-dollar market caps, and boast Sturdy Purchase consensus scores from the Avenue’s finest skilled analysts. So, let’s give two of them a better look.

Microsoft Company (MSFT)

First up on our record is Microsoft, one of many best-known model names on this planet – and likewise the second-largest publicly traded firm on this planet, with a market cap of $1.78 trillion. Microsoft acquired its begin again within the mid-70s, and was a part of the preliminary growth of the non-public pc tech revolution. The corporate rose to prominence when its Home windows working system turned the business commonplace, nonetheless used right this moment, for almost all of all private computing.

Right now, the corporate is adapting efficiently to the rising cloud computing setting, providing merchandise comparable to Workplace 365, which brings the Workplace purposes for dwelling, college, and small enterprise use onto the cloud; Dynamics 365, which does the identical for enterprise purposes; and the Azure platform to assist cloud computing operations. On the similar time, the corporate maintains service and assist for its extra trendy Home windows working techniques.

Within the final reported quarter, Q1 of fiscal 12 months 2023 (September quarter), Microsoft reported $50.1 billion on the high line. This translated to a ten% enhance year-over-year, and beat the $49.6 billion forecast. The strong outcome got here on the again of a 24% reported enhance in cloud income, to $25.7 billion, or barely greater than half of the entire.

On the damaging aspect, the corporate reported a y/y drop in web earnings, by 14% to $17.6 billion, with the diluted EPS falling 13% to $2.35 per share. The true hit for buyers got here from the corporate’s fiscal Q2 steerage, which was set at $52.35 billion to $53.35 billion, or up 2% on the midpoint. This was, nevertheless, beneath the $56.05 billion analysts had needed to see – and the inventory fell after the earnings launch.

Morgan Stanley's Keith Weiss, nevertheless, stays bullish on the corporate's prospects. The 5-star analyst writes, “Whereas buyers fear ahead numbers haven't been de-risked, we see a robust (and sturdy) demand sign within the business companies, which ought to result in enhancing income and EPS progress in 2H23…. The energy of Microsoft's positioning throughout key secular progress segments stays unchanged. Combine shift towards sooner rising Azure and Dynamics 365 and comparatively sturdy Workplace 365 progress (in fixed forex) assist assist administration's objective of 20% fixed forex progress throughout its Business companies.”

In Weiss’s view, Microsoft’s potential absolutely deserves its Chubby (Purchase) score, and his $307 worth goal implies a one-year upside potential of 29%. (To observe Weiss’s monitor document, click here)

General, Microsoft inventory has picked up 27 current scores from Wall Avenue’s analysts, a complete that features 25 Buys towards simply 2 Holds – for a Sturdy Purchase consensus score. The shares are priced at $238.73, and their common goal of $291.34 suggests a 22% acquire on the one-year time horizon. (See MSFT stock analysis on TipRanks)

Alphabet, Inc. (GOOGL)

Subsequent up is Alphabet, the guardian firm of Google, that everybody is aware of. The world’s largest search engine is a part of an general agency that boasts a $1.16 trillion market cap, making it the third largest publicly traded agency, after Microsoft and Apple. Alphabet isn’t simply Google; the corporate additionally owns the Android OS, the favored YouTube web site, and is even transferring into the autonomous car area of interest by means of its Waymo subsidiary.

Whereas Alphabet stays close to the highest of the worldwide tech business, the current 3Q22 confirmed some cracks that can should be addressed. For essentially the most half, these are associated to basic financial circumstances, significantly shrinking promoting budgets within the on-line business. The corporate’s Q3 outcomes confirmed complete revenues of $69.09 billion, up 6% year-over-year – however that modest progress represents a definite deceleration from the prior 12 months’s 41% progress charge, and it missed the $70.5 billion forecast. Working margins additionally fell, from 32% one 12 months in the past to 25% within the final quarter; working earnings was down 18% to $17.13 billion.

The miss in income was exacerbated by a big miss in YouTube’s high line. Promoting income on the video web site got here in at $7.07 billion, lacking the $7.42 billion forecast by a 4.7% margin.

Whereas there are critical headwinds dealing with Alphabet/Google, we must always not underestimate the corporate’s clear strengths. Google stays the web’s premier search engine, and Google Search accounted for greater than $39.5 billion of the entire income. And, regardless of the pullback in general internet marketing, Google Adverts noticed income’s absolute numbers develop by $1.3 billion y/y, to $54.4 billion (a complete that features Google Search’s acquire, in addition to the pullback in YouTube promoting). Lastly, the corporate boasts deep pockets, with over $21.9 billion in money belongings available. Briefly, Alphabet has each the market place and the assets to climate a storm.

Mark Mahaney, 5-star analyst with Evercore ISI, is cognizant of GOOGL’s difficulties within the on-line advert section going ahead. But, whereas he predicts quick time period ache he additionally sees long run acquire: “For now, we estimate GOOGL’s natural income progress deteriorating additional to six% Y/Y in This fall, earlier than starting to get well someday in ‘23. However after the Macro and the FX and the Comps, we strongly imagine GOOGL will re-emerge because the broadest, strongest world advert income platform, with a dramatically worthwhile enterprise mannequin, notable diversification into Cloud Computing, and substantial long-term choice worth with Waymo.”

Quantifying his stance on GOOGL, Mahaney charges it as Outperform (a Purchase) for the 12 months forward and backed by a $120 worth goal that means a 34% upside potential from present ranges. (To observe Mahaney’s monitor document, click here)

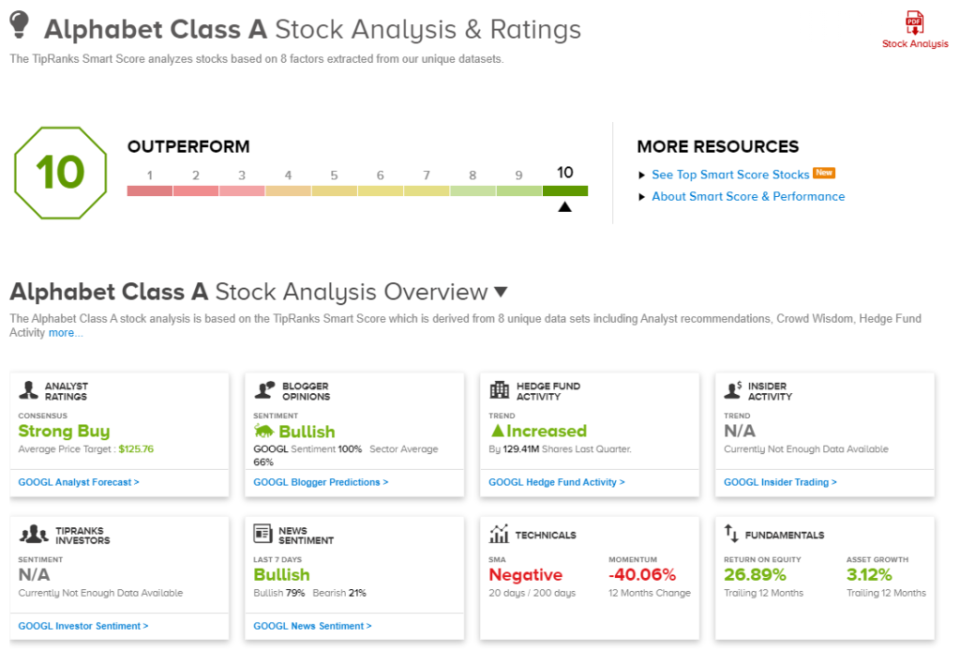

All of Mahaney's colleagues agree together with his thesis. GOOGL shares rating a unanimous Sturdy Purchase consensus score, primarily based on 29 current constructive analyst critiques. The inventory’s common worth goal, $125.76, signifies potential for 41% progress from the present buying and selling worth of $89.23 over the approaching 12 months. (See GOOGL stock analysis on TipRanks)

Keep abreast of the best that TipRanks' Smart Score has to supply.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is vitally necessary to do your personal evaluation earlier than making any funding.