Wilt Chamberlain holds the NBA document for profession rebounds, with 23,924 in complete, or 22.9 per sport, for a very nice sustained efficiency. However rebounds don’t solely are available in basketball, and a savvy investor, whereas not prone to choose up 23,924 rebounding inventory transactions, can nonetheless discover loads of shares which can be primed for rebounds within the present market setting.

That setting, with headwinds nonetheless in play making each shot tougher, has left loads of essentially sound shares undervalued, down from their peaks, generally by 50% or extra. In accordance with Wall Road’s analysts, these are the alternatives that traders must be searching for

We’ve made a begin on it, utilizing the TipRanks platform to find three shares with beaten-down costs however strong prospects for the long run. In accordance with the info, every of those has fallen greater than 50% in latest months, however every additionally has a ‘Robust Purchase’ consensus ranking from the analysts and boasts loads of upside potential. In actual fact, sure Road analysts see all three posting triple-digit positive aspects over the approaching 12 months. Listed here are the small print.

Sunrun, Inc. (RUN)

Let’s begin with Sunrun, an organization within the residential solar energy area of interest that provides prospects a variety of choices for home-based solar energy installations. These are bundle offers, customized made for every buyer’s house, and embody every little thing wanted to make an ideal match to the client’s specific location and energy wants. Sunrun can deal with every little thing concerned within the set up, from organising the rooftop photovoltaic panels to putting in energy storage batteries and sensible management programs, to connecting the photo voltaic set up to the native energy grid.

Along with providing a full-service photo voltaic set up, Sunrun additionally affords a number of financing choices. Clients can select from paying the complete value up entrance, to personal the system fully, or can amortize it as a lease, on a long-term or a month-to-month foundation. The corporate may also present loans to make the installations inexpensive. The corporate’s mixture of full residential installations and versatile financing have attracted some 700,000 prospects, unfold throughout 22 states, plus DC and Puerto Rico.

Within the lately reported 1Q23 print, Sunrun confirmed a number of necessary development metrics. The corporate reported 240 complete put in megawatts for the quarter, beating the excessive finish of its beforehand printed steerage, and an total 30% enhance year-over-year in gross sales actions. In California alone, the corporate reported 80% y/y development.

Attending to the agency’s monetary outcomes, we discover that Sunrun had a combined quarter. The highest line was up, with the $589.85 million in reported income rising 19% y/y and beating the forecast by over $72 million. On the backside line, nonetheless, the corporate’s EPS of -$1.12 missed expectations by $0.97. Sunrun reported $1.1 billion annual recurring income, and a median contract lifetime of 17.6 years, each metrics that bode nicely going ahead.

General, it’s necessary to notice that Sunrun inventory has skilled a major decline of 57% from its peak in September.

However, following the Q1 print, Evercore ISI analyst James West sees the inventory as primed to say again these losses and lays out the bull-case. He writes, “RUN continues to expertise robust momentum throughout all of its gross sales channels and is increasing its buyer worth proposition. The corporate grew photo voltaic power capability put in by 12% YoY and reiterated its steerage for no less than one other 10-15% development in 2023. This may equate to including over 1 GW of capability this 12 months, the equal of a median nuclear energy plant which takes a long time to construct.

“As well as,” West went on to say, “there may be doubtless upside to this forecast pushed by when the Treasury gives additional steerage on the ITC (funding tax credit score) adders that are solely out there with the subscription mannequin, growing battery connect charges and its new Shift providing, working by means of its elevated pipeline from robust CA buyer development within the first quarter forward of the web metering adjustments, and potential market share positive aspects as the combination continues to shift to its subscription mannequin.”

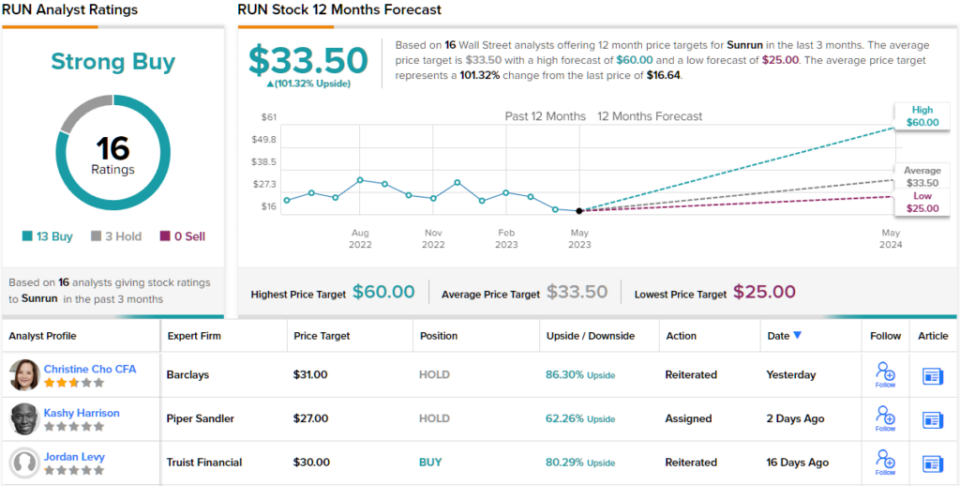

To this finish, West provides RUN shares an Outperform (i.e. Purchase) ranking, with a $60 value goal to counsel a robust one-year upside of ~261%. (To look at West’s tack document, click here)

General, the Road’s outlook on Sunrun is a Robust Purchase, supported by 15 latest analyst evaluations that embody 12 Buys and three Holds. The shares are at present buying and selling for $16.64 and have a median value goal of $33.50, indicating room for ~101% development within the subsequent 12 months. (See Sunrun stock forecast)

OptimizeRx Company (OPRX)

Subsequent up is OptimizeRx, an organization that brings digital tech to the sphere of healthcare. The agency gives a platform to attach the details of the healthcare business – suppliers, sufferers, and amenities – to create a seamless community of mutually accessible data and prepared solutions. The tip result's a healthcare course of that delivers extra exact and extra environment friendly care, on to the affected person.

OptimizeRx’s platform affords completely different options for sufferers and suppliers, primarily based on what’s wanted. For sufferers, the options middle on communications with physicians and different suppliers, supporting affected person engagement with therapy, and sustaining compliance with privateness rules. For suppliers, the platform contains affected person communications, however focuses on streamlining affected person document preserving, sustaining contact with take a look at labs, hospitals, and specialists, monitoring and monitoring prescriptions, and coordinating discharge companies.

General, this firm has made good penetration into the US healthcare discipline. Its community is linked to greater than 300 digital well being document programs, and the corporate can attain greater than 60% of ambulatory prescribers. OptimizeRx has reported some actual successes, together with an 86% doctor engagement with the system’s messaging, and a 12% enhance in remedy days for sufferers coping with continual circumstances.

The agency’s This autumn financials are usually the 12 months’s greatest, so a dropoff in Q1 was anticipated – however nonetheless, the lately launched Q1 outcomes have been decidedly combined. In 1Q23, the highest line income of $13 million was down 5.3% y/y however beat the forecast by nearly $648,000. On the backside line, the adj. EPS lack of 9 cents was deeper than the 8 cents anticipated, and in contrast poorly to the year-ago interval’s 1-cent EPS loss.

Shares dropped following the quarterly readout, and in complete, they're down 51% within the final 12 months.

Regardless of the combined financials and the decrease share value, this inventory stays essentially engaging within the eyes of Roth MKM analyst Richard Baldry. He writes: “1Q22 outcomes have been honest, with a modest yr/yr income decline as seen in 2H22, however with reiterated steerage implying a near-term (we mannequin 2Q23) return to optimistic development and 10%+ income development total for 2023. Importantly, 1Q23 revenues narrowly beat our forecast and hit the high-end of steerage to sign larger administration visibility into underlying demand. With shares already far under their 2021 highs, we imagine the danger/reward outlook has turned meaningfully optimistic.”

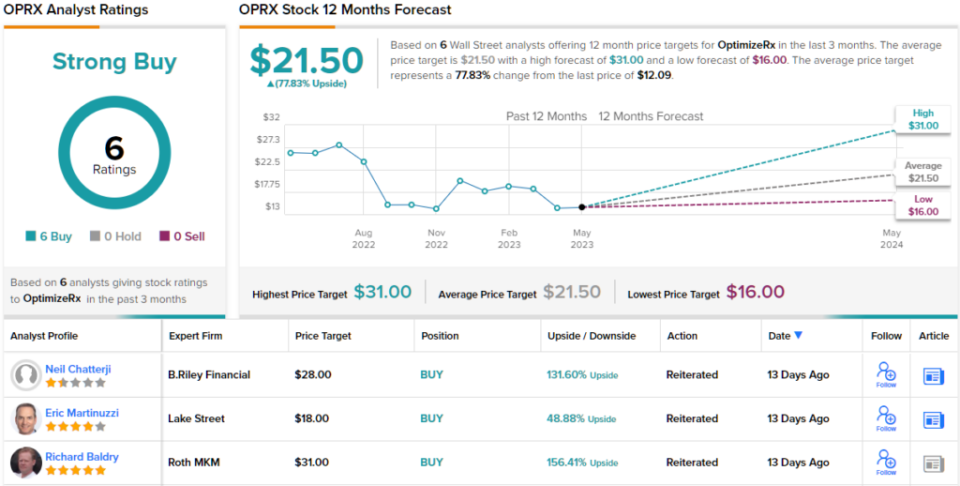

Baldry makes use of this stance to again up his Purchase ranking, and his $31 value goal implies a sturdy 156% upside on the one-year horizon. (To look at Baldry’s monitor document, click here)

The Road is clearly within the bulls’ nook on this one, because the Robust Purchase consensus ranking, primarily based on 6 optimistic analyst evaluations, is unanimous. Shares are buying and selling for $12.09, and the $21.50 common value goal suggests a 78% enhance from that stage within the 12 months forward. (See OPRX stock forecast)

Largo Sources (LGO)

Final on our beaten-down record is Largo Sources, a pacesetter within the transfer in direction of decreasing carbon emissions and power use within the sector. Particularly, Largo is a world chief within the manufacturing of vanadium batteries and sources its vanadium steel from the Maracas Menchen mine, which it owns. Situated in Brazil, the mine accommodates high-grade vanadium deposits crucial for the manufacturing of vanadium batteries. These batteries supply a lifespan of 25+ years and supply a protected and environment friendly recycling course of on the finish of their life. Largo’s batteries are discovering purposes for long-term power storage within the US power business.

Vanadium is taken into account a uncommon earth steel, and Largo’s mine is without doubt one of the world’s main sources. The corporate produces two fundamental vanadium merchandise from the mine. The primary is VPURE+ Flakes, high-grade vanadium flakes with a purity stage of 99% or larger, utilized in grasp alloy manufacturing. These flakes enhance the strength-to-weight ratios of titanium alloys used within the aerospace business. The second chief product from the mine is VPURE+ vanadium pentoxide powder. This product, additionally with a purity stage of 99%, is utilized in catalyst and battery purposes. Largo is engaged on enhancing its mine operations by means of infill drilling at its Campbell Pit mission.

Along with its vanadium operations, Largo is within the means of commissioning a serious ilmenite focus plant, deliberate for opening this 12 months. Ilmenite is a titanium-iron oxide mineral with varied makes use of, together with the manufacturing of paints, inks, materials, plastics, paper, and even sunscreen and cosmetics. The corporate plans to enhance its vanadium enterprise with ilmenite manufacturing.

Concerning monetary outcomes, Largo reported revenues of $57.4 million in Q1 of this 12 months, representing a 35% year-on-year enhance and surpassing analyst forecasts by $3.27 million. The rise in income was attributed to larger vanadium costs within the international market. Nonetheless, the underside line confirmed a internet loss, with an EPS determine of -$0.02. Whereas this was an enchancment in comparison with the lack of 3 cents within the year-ago quarter, it fell 4 cents under expectations. The corporate reported strong vanadium manufacturing throughout Q1, extracting a complete of 341,967 metric tons of ore from the bottom, which marked a major enhance from the 303,652 metric tons produced in the identical interval final 12 months.

In these final 12 months, nonetheless, Largo’s shares are down 56%.

That hasn’t bothered H.C. Wainwright analyst Heiko Ihle, who says of Largo: “We stay optimistic about Largo’s vanadium operations as market fundamentals proceed to stipulate appreciable long-term demand development although spot pricing has been fairly lackluster as of late.”

Placing some numbers the place his mouth is, Ihle provides LGO shares a $12 value goal, suggesting ~208% upside within the subsequent 12 months, and supporting his Purchase ranking. (To look at Ihle’s monitor document, click here)

General, this inventory has picked up 4 analyst evaluations lately, they usually favor Buys over Holds by a 3 to 1 margin – for a Robust Purchase consensus ranking. The inventory is promoting for $3.90, and its $8.80 common value goal suggests it has room to develop ~126% within the 12 months forward. (See LGO stock forecast)

To search out good concepts for shares buying and selling at engaging valuations, go to TipRanks’ Best Stocks to Buy, a newly launched software that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is rather necessary to do your individual evaluation earlier than making any funding.